Yesterday, the Federal Open Market Committee (FOMC) announced "Operation Twist II" under economic conditions described well in an many places virtually every day, including this very blog (e.g., "GDP Slide Signals Recession. Soon.").

There are similarities and differences in the U.S. economic conditions existing during the two periods. One obvious similarity centers on the status of the business cycle, meaning the above-referenced R-word was or is on almost everybody's lips in both cases. One obvious difference centers on the country's debt as a percentage of gross domestic product, which was not too bad in 1961 but is not too good in 2011.

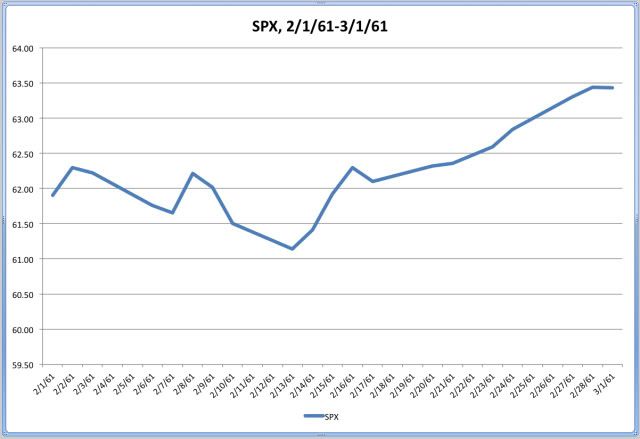

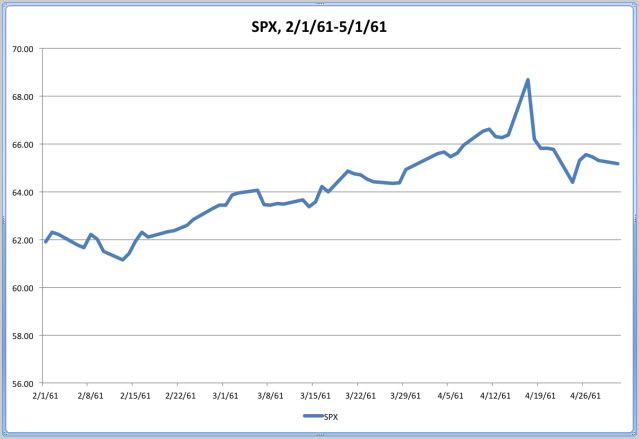

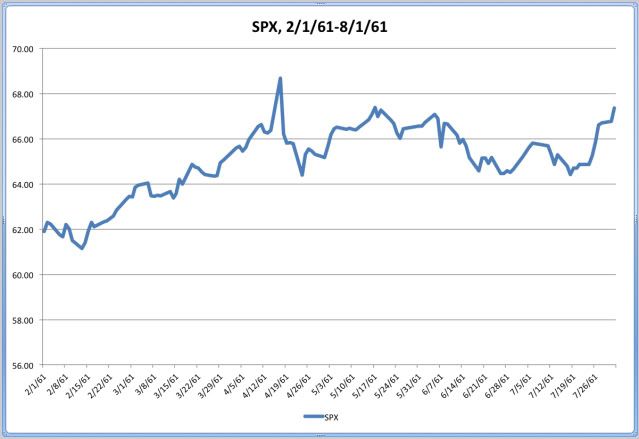

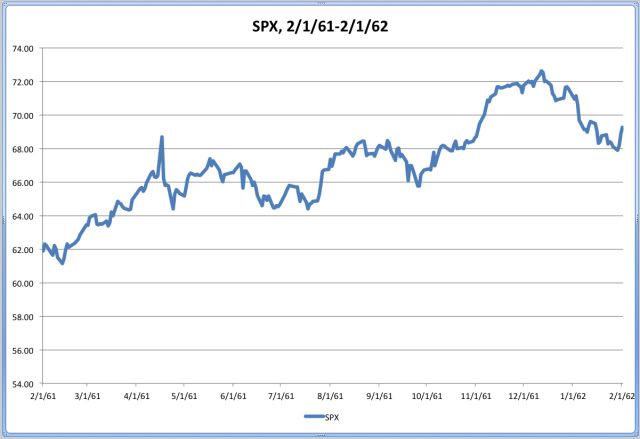

Given this mishmash, it may or may not be helpful to examine the market performance of the Standard & Poor's (S&P) 500 (SPX) in the wake of the launch of "Operation Twist I" on Feb. 2, 1961. But I did it, anyway.

With a common baseline of Feb. 1, 1961, the four charts below show the S&P 500's behavior during the following one-month, three-month, six-month, and one-year periods, respectively:

Source: Risky Business Charts Based on Yahoo! Finance Adjusted Closing-Price Data

If past is prologue, then the recent equity-market crash may be comparatively short-lived. After all, the Fed will be driving financial-market participants out of the long end and into the short end of the U.S. Treasury yield curve, as well as higher-risk assets.

If past is not prologue, then the recent stock-market crash may be relatively long-lived. Clearly, aggregate demand is lacking in the U.S., and nearly all available evidence indicates this circumstance is other than either a local or a temporary phenomenon.

You pays your money, and you takes your chances.

{kind=link}