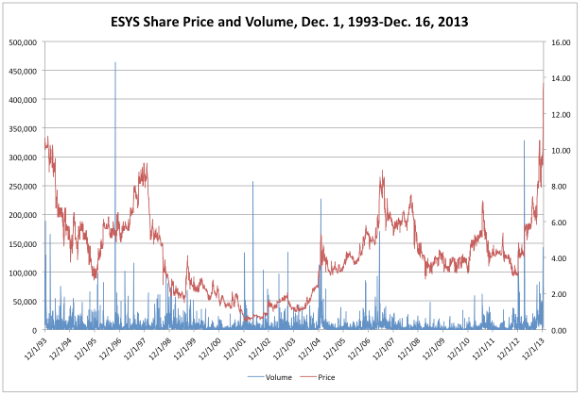

Sooner or later, the Elecsys

Corp. (ESYS)

will come to the end of the parabolic move in its share price that began after

the company reported before the equity-market open Dec. 9 the excellent financial

results for its 2014 fiscal year’s second quarter, which concluded Oct. 31.

Animal spirits in the stock market subsequently drove the electronic-equipment

firm’s closing share price fast and furiously to an all-time high of $13.70 on

Dec. 16 from $9.54 on Dec. 6, a gain of $4.16, or 43.61 percent.

Based on the fundamental valuation of ESYS, one could

anticipate the culmination of its parabolic move this week. But Elecsys is a

micro-capitalization company, with the 3,806,968 shares outstanding giving it a

current market cap of about $50.37 million, based on the share count in the

U.S. Securities and Exchange Commission Form

10-Q the firm filed the same day it delivered its quarterly financial

report. Decembers being Decembers and micro-caps being micro-caps, it is

therefore conceivable the stock could run higher and longer than otherwise would

be the case.

Such an additional run may not be backed by the fundamental

valuation of Elecsys, but it might be supported by the nature of the company’s

ownership. Insiders hold about 33.07 percent of the shares, while institutions

hold about 4.26 percent of them, according to Nasdaq.com.

Meanwhile, ESYS short interest was negligible Nov. 29, with just 2,483 shares

held short then, the same

source reported. Of course, this figure most likely will rise in December,

especially given the fact ESYS is not an optionable stock.

Source: This chart is

based on ESYS share-price and -volume data at Yahoo! Finance.

The Business of

Elecsys

Elecsys offers so-called machine-to-machine (M2M)

communication-technology solutions, data-acquisition and -management systems,

and electronic equipment for industrial applications on a global basis. Based

in Olathe, Kan., the company has described its primary markets as being in

agriculture, energy production and distribution, safety and security systems, transportation,

and water management. In serving those markets, the firm furnishes wireless remote

monitoring, mobile computing, industrial data communication, and custom electronic-manufacturing

services encompassing assemblies and displays.

Color on one of Elecsys’ lines of business was provided in its

Aug. 1 announcement

of a $1.25 million order placed by the Al Rushaid Group to supply remote

monitoring equipment for deployment in the Ghawar oil field of Saudi Arabia.

The company reported its equipment would enable remote monitoring of

cathodic-protection-system performance at about 600 seawater injection wells in

the mammoth oil field, commonly described as the largest conventional oil field

in the world. The firm’s equipment would be installed as part of a project to

employ smart oil-field technologies to extract resources more efficiently and maximize

production.

In its latest SEC Form 10-Q, Elecsys reported the revenue

and gross margin for each of two business segments: proprietary M2M products

and services on the one hand and original equipment manufacturer (OEM) custom

solutions on the other hand.

During Q2, the company’s revenue for proprietary M2M

products and services advanced to $3,742,000 this fiscal year from $3,148,000

last fiscal year, an increase of $594,000, or 18.87 percent. The gross margin

for this segment was 51.74 percent, compared with a reported 53.00 percent in

the same quarter a year ago.

Over the same period, the firm’s revenue for OEM custom

solutions climbed to $3,588,000 from $2,990,000, an increase of $598,000, or

20.00 percent. The gross margin for this segment was 30.43 percent, compared

with a reported 24.80 percent in the same quarter a year ago.

Elecsys reported its overall Q2 revenue rose to $7,330,000

this fiscal year from $6,138,000 last fiscal year, an increase of $1,192,000,

or 19.42 percent. On the same basis, the company said its earnings per share

surged to 17 cents from 11 cents, an increase of 6 cents, or 54.55 percent. The

firm’s overall gross margin was 41.31 percent, compared with a reported 39.30

percent in the same quarter a year ago.

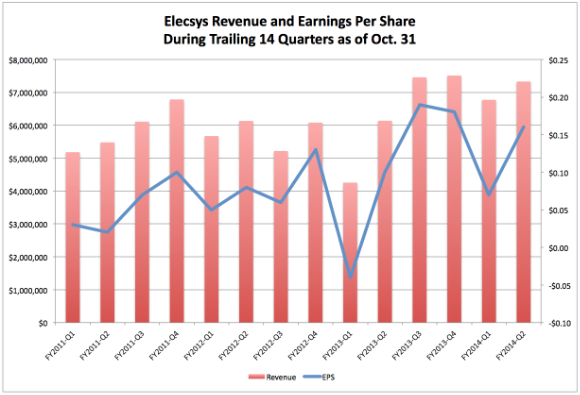

Elecsys has been profitable for five consecutive quarters

and for three straight fiscal years, as illustrated by the below chart. The

company most likely will be profitable again this fiscal year, with EPS of 23

cents already booked in the first half and the firm saying in its most recent Form

10-Q, “Although the current period did not contain revenue from the previously

announced order from the Al Rushaid Group in Saudi Arabia, due to a delay by

the prime contractor, we expect a positive impact on revenues from this order

over the next two fiscal quarters.”

Source: This chart is based

on figures in Elecsys’ relevant SEC

filings.

The Valuation of

Elecsys

If I had to employ one single solitary word to describe the

spark that set ESYS ablaze at the outset of the stock’s parabolic move last

week, then it would have to be Backlog.

In the incendiary context of the Elecsys Q2 financial report, its EPS was the

fuel, and its revenue was the kindling, but its backlog was the tinder.

The Q2 backlog scheduled for delivery during the ensuing 12

months advanced to $12,423,000 this fiscal year from $10,638,000 last fiscal

year, an increase of $1,785,000, or 16.78 percent. To put this backlog in

perspective, it helps to know the company’s overall revenue in the 2014 fiscal

year’s first half was $14,104,000. By segment, the Q2 backlogs were $10,332,000

for OEM custom solutions and $2,091,000 for proprietary M2M products and

services.

As ESYS’ recent share-price action has shown, equity-market

participants really and truly value this kind of visibility.

OK, the Elecsys Q2 backlog and income statement appeared flat-out

great, but neither its cash-flow statement nor its balance sheet seemed so. One

reason is the explosive growth in the company’s net inventories, which soared

to $8,447,000 in Q2 from $6,837,000 in Q1, an increase of $1,610,000, or 23.55

percent, as illustrated by the below chart.

Historically, I believe, rising inventories (or supply) have

been either a coincident or a leading indicator of unexpectedly falling revenue

(or demand), and falling inventories have been either a coincident or a leading

indicator of unexpectedly rising revenue. In this case, however, I think

Elecsys’ bloated net inventories mostly reflect the company’s readiness to

deliver on its backlog in general and the Al Rushaid Group order in particular.

Because the firm is a micro-cap, there is no analyst coverage to use as a

reality check in this circumstance.

Elecsys’ net inventories are one thing; its indebtedness is

another. In my analysis of the company’s balance sheet at the close of Q2, I

began with $501,000 in cash and cash equivalents, subtracted $7,058,000 in

total liabilities, and divided by 3,806,968 shares to produce net cash per

share of -$1.72. It is true the firm’s latest SEC Form 10-Q has reported $1,842,000

of its liabilities will not have to be paid until after 2018, and it is true its

current ratio is 3.22, but it is equally true I do not like any figure on net

cash per share to begin with a minus sign.

Given ESYS’ parabolic move, it is unsurprising the stock

appears either fully valued or overvalued in an MSN

Money comparison of four key price ratios centered on it and the

contract-manufacturers industry averages, as well as in a comparison with my

own estimate. Before the stock-market open Tuesday, Elecsys looked more expensive than

the industry average by their respective price-to-book value ratios, 3.60

versus 1.53; price-to-cash flow ratios, 42.92 versus 4.81; price-to-earnings

ratios, 22.83 versus 20.53; and price-to-sales ratios, 1.84 versus 0.26. Of

course, the company has better-than-average gross, pretax, and net profit

margins, which account for a piece of its premium price.

Source: This chart is based

on figures in Elecsys’ relevant SEC

filings.

Elecsys and the

Incredible Shrinking Share Count

The number of ESYS shares outstanding is already low, but Elecsys

has a stock-buyback

program in place that could drive this number even lower. According to the

company announcement of the program exactly one year ago, its directors OK’d

the repurchase of as much as 10 percent of the firm’s shares, or 400,000

shares. Providing for the buyback of stock from time to time at prevailing

market prices through either open-market or privately negotiated transactions,

the program has no expiration date.

Based on an analysis of the relevant SEC forms filed between

then and now, I believe Elecsys repurchased 130,774 shares at an average price

of $5.87 and a total cost of about $767,464.50 under the program as of Oct. 31.

Given the company’s debt load and equity structure, certain growth-and-value

investors may wonder whether this approach has resulted in the best allocation

of capital during the past year. This wonderment aside, the firm’s Q2

repurchases of 55,093 shares at an average price of $7.14 and a total cost of about

$393,000 may point to a target it would be willing to defend once the ESYS

parabolic move is over.

Regardless of its share count, the micro-cap Elecsys has to effectively

face different competitors in its different lines of business, as noted in the SEC

Form

10-K it filed July 10. Among these mostly large-cap rivals are Honeywell

International Inc. (HON)

and Motorola Solutions Inc. (MSI)

in the area of mobile computing; the Cooper Industries unit of Eaton Corp. PLC

(ETN),

the Emerson Electric Co. (EMR),

and Siemens AG (SI)

in the area of industrial data communication; and Celestica Inc. (CLS),

Flextronics International Ltd. (FLEX),

and the Sanmina Corp. (SANM)

in the area of electronic-manufacturing services.

The company also has to avoid the concentration of risk represented

by a comparatively small customer base, as pointed out in its Form 10-K. The

firm’s five biggest customers accounted for 53 percent of revenue in the 2013

fiscal year and 43 percent of it in the 2012 fiscal year. During the same two

periods, its largest customer accounted for 30 percent and 20 percent of

revenue, respectively.

Many risks associated with Elecsys as either an investment

or a trading vehicle are well described on pages 11-15 of the company’s Form

10-K. One risk unmentioned there centers on ESYS’ status as a micro-cap stock:

Almost by definition, this means the equity’s points of entry and exit are

similar in size (i.e., it may difficult to get in at a reasonable price and it

may difficult to get out at a reasonable price). A few risks associated with

anything as either an investment or a trading vehicle include changes in the loose-money

policies of the U.S.

Federal Reserve and other central banks around the world. Along this line,

it is important to note the Federal Open Market Committee will conduct its first

meeting of next year on Jan. 28-29.

A hat tip and thanks

to Seeking Alpha commenter Hal44, who mentioned ESYS last week (before the

stock’s parabolic move).

Disclaimer: The opinions

expressed herein by the author do not constitute an investment recommendation,

and they are unsuitable for employment in the making of investment decisions.

The opinions expressed herein address only certain aspects of potential

investment in the securities of any companies mentioned and cannot substitute

for comprehensive investment analysis. The opinions expressed herein are based

on an incomplete set of information, illustrative in nature, and limited in

scope, and there are limitations to their accuracy. The author recommends all

investors conduct detailed investment research of their own, including review

of relevant SEC filings and consultation with a qualified investment adviser.

The information upon which this article is based was obtained from sources

believed to be reliable, but it has not been independently verified, which

means the author cannot guarantee the accuracy of this information. In

addition, the opinions expressed herein reflect the author’s best judgment as

of the date of publication, and they are subject to change without notice.