Because I have been an editor/writer almost all my life, it is my conceit that words -- and the meanings of words -- are more important to me than they are to most equity-market operators.

I therefore have strict definitions of stock-market terms such as Consolidation, Correction, Bear Market, and Bull Market in the current context of the S&P 500, as follows:

Consolidation: Bringing into play the SPX cyclical high level of 1,370.58 on May 2, I believe the index entered a consolidation phase when it moved below 1,302.05 on June 3.

Correction: Employing the same cyclical high level, I think the S&P 500 entered a correction phase when it moved below 1,233.52 on Aug. 4.

Bear Market: Using the same cyclical high level, I believe the birth of the index's new bear market was confirmed when it moved below 1,096.46 today.

Bull Market: Likewise, I think the death of the SPX's old bull market was confirmed when it moved below the same value today.

Given this confirmed change in character, I consider one of my main tasks as an equity-market operator centers on the identification of likely areas of support and resistance -- not only for individual issues but also for major stock-market indices.

In doing so, I conduct analyses of the U.S. economy on the one hand and analyses of the fundamental, sentimental, and technical conditions of the U.S. markets on the other hand.

Day in and day out, I count my study of Fibonacci retracements (FRs) across multiple time frames as surprisingly helpful. I employ the term surprisingly because if Fibs are proven to have any prognostic value in the equity market, then I personally would attribute the phenomenon to self-fulfilling prophecy more than to anything else.

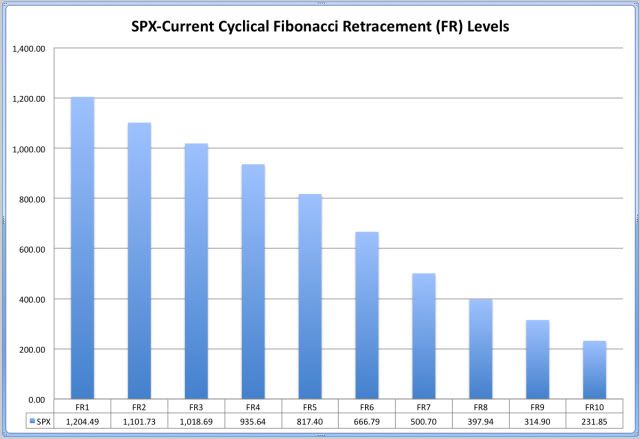

Even so, I appreciate the insights provided by my study of cyclical FR levels of the S&P 500 -- and other indices -- especially since the market-volatility storm began to rage in earnest on Aug. 4. And the following chart focusing on the SPX shows why:

Looking backward, I note there were 42 trading days between Aug. 4 and Oct. 3, inclusive. The S&P 500's closing level on 35 days (83.33%) fell in the range from FR1 (1,204.49) to FR2 (1,103.73). The SPX closed above FR1 on five days (11.90%), at FR1 on one day (2.38%), and below FR2 on one day (2.38%). As a guide to support and resistance, the cyclical Fibs appear to have done yeoman work to this point in the market-volatility storm.

Looking forward, I suspect it is more likely than not the S&P 500 will visit the area of FR3 (1,018.69), sooner or later.

Methodological Note:

I calculated my FR levels employing the 666.79 intraday value recorded March 6, 2009, as the relevant cyclical trough and the 1,370.58 intraday value recorded May 2 of this year as the relevant cyclical peak. Below are my FR levels and their corresponding percentages:

FR1: 23.60%

FR2: 38.20%

FR3: 50.00%

FR4: 61.80%

FR5: 78.60%

FR6: 100.00%

FR7: 123.60%

FR8: 138.20%

FR9: 150.00%

FR10: 161.80%

No comments:

Post a Comment